Introduction

Auto insurance is a must—but overpaying isn’t. From safe driving to smart shopping, there are multiple ways to reduce what you spend without putting yourself at risk. In this post, we share actionable tips that can lead to serious savings.

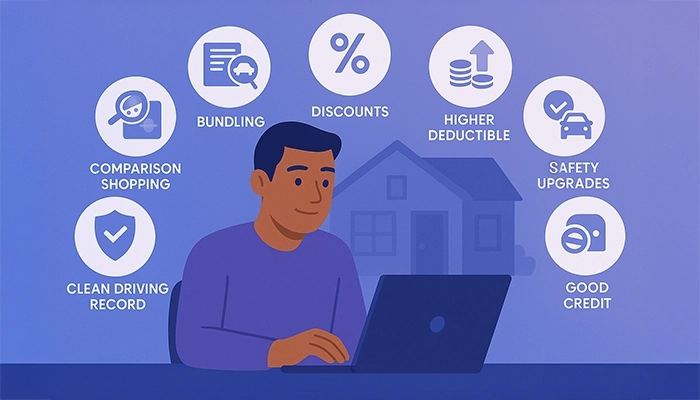

1. Compare Quotes Regularly

Prices vary between providers. Shop around at least once a year, especially if your circumstances have changed.

2. Bundle Your Policies

Many insurers offer discounts when you combine auto with homeowners, renters, or life insurance.

3. Take Advantage of Discounts

Ask about:

- Safe driver discounts

- Good student rates

- Defensive driving course completion

- Anti-theft and safety feature credits

4. Raise Your Deductible

Opting for a higher deductible on comprehensive and collision coverage can lower your premium. Just make sure you have the savings to cover it if needed.

5. Drive Less, Pay Less

If you work from home or drive under 7,500 miles annually, you may qualify for a low-mileage discount.

6. Maintain a Clean Driving Record

Avoiding tickets and accidents over time helps keep your rates low. One incident can raise rates for years.

7. Improve Your Credit Score

In most states, insurers consider credit when setting premiums. Better credit often means better rates.

Conclusion

Cutting your insurance costs doesn’t mean cutting corners. Use these tips to keep your coverage strong and your bill low. And don’t forget to use our Auto Insurance Premium Calculator to estimate your savings.

FAQ:

Q: How often should I shop for new auto insurance?

A: Every 6 to 12 months, or any time your life changes significantly.

Q: Is it better to pay monthly or in full?

A: Paying in full often results in discounts.

Q: Will my rate go down if I don’t file claims?

A: Yes, many insurers reward claim-free driving with lower rates.